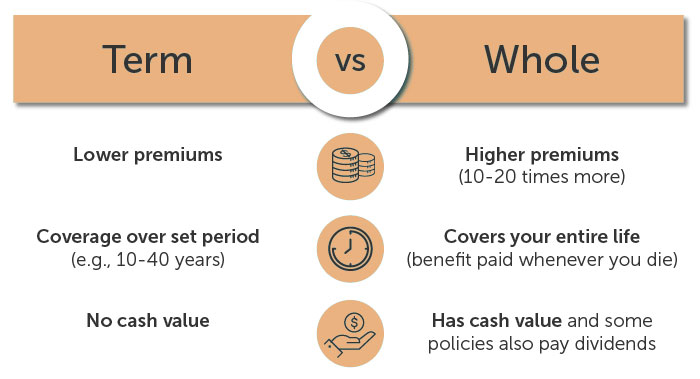

How do I protect my kids or Spouse? Whether you’re a Veteran looking for lower cost Life Insurance, a Nurse with long daily commutes or simply the breadwinner taking care of a family. People depend on you and your income. If that goes away, where does that leave them? Providing a safety net is easier than you think. Giving them time to adjust financially is the solution. With a Term policy in place, the payout to your beneficiary will go to good use serving as a buffer for funeral costs, emergency savings or just a way to plan for a transitional period.